|

New technologies, such as artificial intelligence (AI) and robotic process automation, blockchain/ distributed ledger technologies, data analytics, and the Internet of Things (IoT; i.e., the integration of sensory and wireless technology into objects, giving them the ability to transmit data about themselves, their condition, and their environment), can be leveraged to enrich the breadth, coverage, and depth of environmental, social, and governance (ESG) due diligence and ESG ratings, and thus build much-needed digital trust. At the national government level, APAC’s largest economies – China, India, Japan, and Korea – have either reaffirmed their previous commitment to carbon neutrality and carbon emission reductions or shared more ambitious goals at the 2021 Summit for Climate Change held on 22–23 April. At the individual level, as a consumer, employee, or investor, what can we do to help fight climate change and significantly contribute to the 17 Sustainable Development Goals (SDGs) proposed by the United Nations? |

|

|

Mr Lapman Lee Professor of Practice (FinTech and Innovation) School of Accounting and Finance |

Vote for ESG with Your Wallet

Because the annual financing gap to achieve the SDGs by 2030 is estimated at US$2.5 trillion, individual and institutional investors can “vote with their wallet” to provide capital to companies (listed and private) to carry out initiatives and projects that are in line with their ESG expectations.

The ESG Data Challenge

With the myriad of ESG-themed debt and equity financial products, you can (1) rely on a company’s self-reported ESG performance, which puts you at risk of greenwashing (the company may create the misleading impression that its products, services, and policies are environmentally friendly, which may not reflect reality); (2) make your investment decisions based on a company’s ESG rating by a third-party provider, in which the breadth and depth of the methodology may vary between providers; or (3) use a combination of the two. Typically, a company’s ESG rating is based on a combination of insights generated from meetings with the company and desktop analysis of its industry and peers, enriched with data from external data providers.

However, supply chains are becoming more complex, global, and dynamic. A company can be exposed to ESG risks without the management’s knowledge via its Tier 1 suppliers (companies that directly supply goods and services) and Tier 2 suppliers (suppliers who supply the Tier 1 suppliers). This poses a challenge for ESG ratings as the rating agencies do not necessarily have timely access to relevant primary and dynamic data to conduct enhanced due diligence to achieve the much-needed transparency and visibility in the end-to-end supply chain, from raw material sourcing processes and suppliers to the health and safety of employees and their human rights.

You may automatically assume that a company that produces electric vehicles has a positive impact on the environment because 1) electric vehicles produce no carbon emissions, and 2) the electricity used is environmentally friendly if it is generated from renewable energy sources. However, further ESG due diligence is warranted to understand the company’s manufacturing processes (energy efficiency, pollution, waste management, and water usage) and people’s labour conditions. In this example, the ESG due diligence assessment of lithium-ion battery manufacturers and suppliers of raw materials, such as lithium and cobalt, may prove useful as the countries that supply the raw materials may not have the same ESG standards as the electric vehicle company.

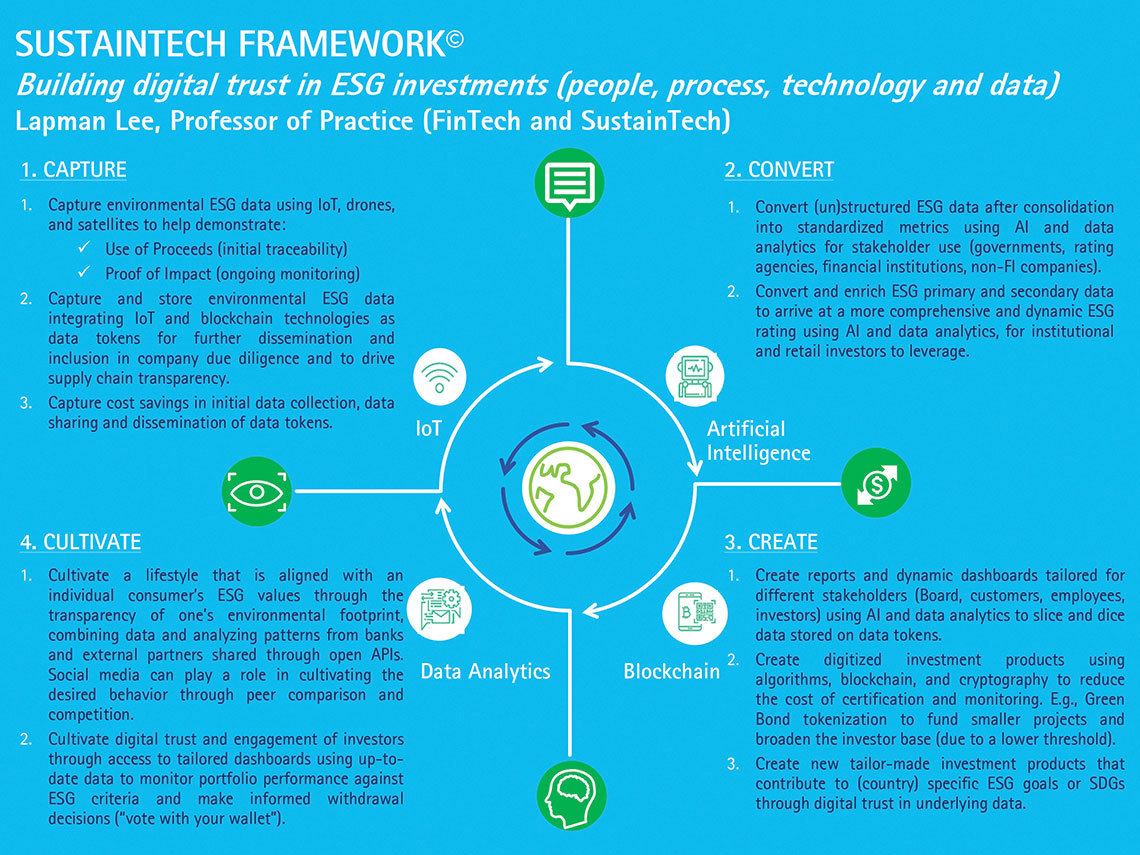

SustainTech Framework

The SustainTech framework presented below illustrates how emerging technologies can help build digital trust in ESG investments in the capture, conversion, creation, and cultivation phases of the process.

Source: SustainTech Framework by Lapman Lee

ESG Digital Trust

Here, digital trust is defined as the degree of trust in the reliability and robustness of the primary and secondary data used to support ESG ratings that leverage technology and ESG due diligence.

- ESG rating of the issuer or of the debt or equity instruments issued

- Supply chain due diligence

- Investment due diligence

- Use of Proceeds: Is the capital invested in the projects and initiatives for which it was intended?

- Proof of Impact: How do you demonstrate the concrete impact of your investment?

In my opinion, building ESG digital trust is a prerequisite to drive capital from individual and institutional investors to companies and projects to meet the UN SDGs by 2030.

Technology plays a key role in providing dynamic and easy-to-use data to make informed ESG investment decisions, monitor ESG performance, and withdraw investments if ESG performance declines, allowing us to truly vote with our wallet.

|

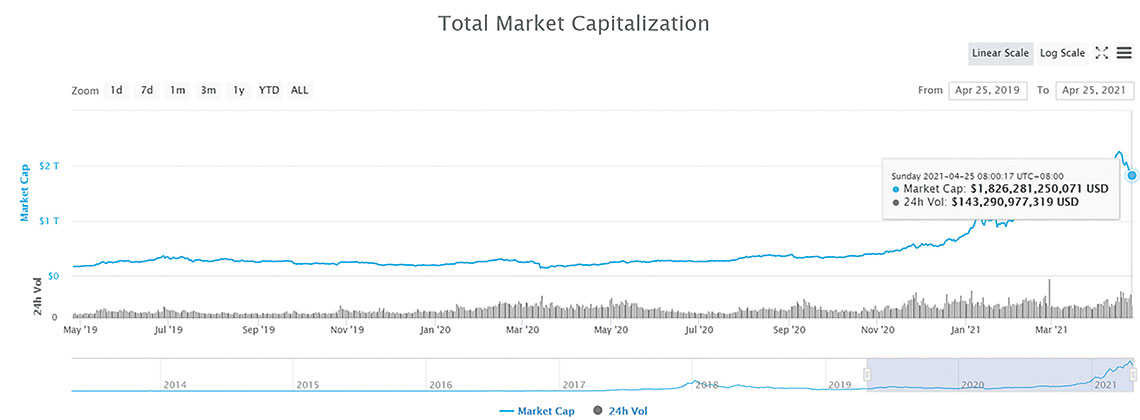

“I own a lot of Ethereum because I think it’s the closest to a true currency”. — Mark Cuban As of 25 April 2021, the total market capitalization of the cryptocurrency market was US$1,826.3 billion. In comparison, the total market capitalization of the US stock market was US$49,107.7 billion, and the total market capitalization of the Hong Kong Stock Exchange was HK$52,062.2 billion (US$6,709.8 billion). Compared with the stock market, the market capitalization of the cryptocurrency market is relatively small (around one third that of the stock market); nevertheless, the cryptocurrency market should not be overlooked in the new digital era. Have you ever traded a cryptocurrency? This article is a quick guide to trading in the cryptocurrency market and hopefully answers some of your questions about the exciting but mysterious opportunities that cryptocurrency trading offers. |

|

|

Dr Jimmy Jin Assistant Professor School of Accounting and Finance |

Figure 1: Total market capitalization of cryptocurrencies

What is a Cryptocurrency?

A cryptocurrency is a type of digital currency secured by cryptography. Many cryptocurrencies are based on blockchain technologies, which use a decentralized network (of computers) to record and transact digital currencies without being controlled by central authorities. Examples of popular cryptocurrencies include Bitcoin, Ethereum, and Filecoin.

Figure 2: A list of popular cryptocurrencies

Are Cryptocurrencies Traded on a Stock Exchange? And How Can I Buy a Cryptocurrency?

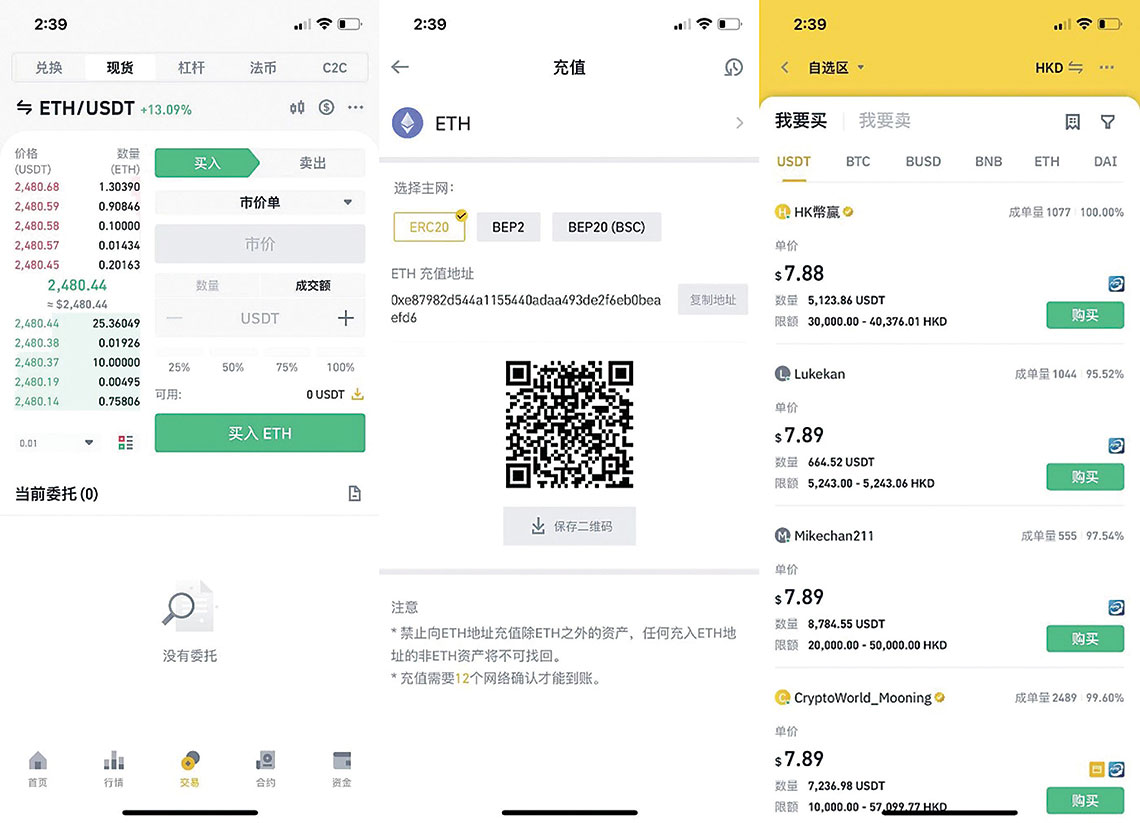

The answer to the first question is yes and no. There are cryptocurrency exchanges, such as Coinbase, Binance, and Huobi Global, operating 24 hours a day, seven days a week. These exchanges provide a platform to trade cryptocurrencies, future contracts, and options with/without margin accounts (see Figure 3). Thus, a quick answer to the first question is yes, you can buy cryptocurrencies on a stock exchange using other cryptocurrencies or fiat money.

Alternatively, you can trade cryptocurrencies directly with other investors, especially as cryptocurrency exchanges are centralized and against the idea of decentralization. You only need a bank account and a cryptocurrency wallet, but cryptocurrency wallet systems are relatively complex, recording full/partial cryptocurrency information online/offline. The first step is to use a wallet provided by an exchange (see Figure 4); however, such a wallet can be stolen as it is online and centralized (i.e., a centralized wallet, which is similar to a bank account). An advanced option is to use Metamask or Binance Smart Chain Wallet (i.e., a hot wallet, which is similar to a personal wallet). Some exchange platforms also offer a client-to-client (C2C) trading option (see Figure 5).

An ongoing revolution in blockchain and cryptocurrency trading is “DeFi”, or decentralized finance. DeFi allows investors to engage in cryptocurrency financial applications aimed at disrupting financial intermediaries. Yield farming is a major application that allows users to stake their cryptocurrencies in exchange for additional rewards. Another important application is the DeFi exchange, sometimes called “cryptocurrency decentralized exchange”, which enables transactions without a centralized middleman (using a hot wallet directly). It is also possible to buy cryptocurrencies using the DeFi network. The mechanism is very similar to C2C trading without a centralized exchange platform.

These days you have another option for cryptocurrency trading, that is, through blockchain exchange-traded funds (ETFs). These new investment vehicles on the traditional exchange are a very convenient way to invest in cryptocurrencies, but note that you do not own cryptocurrencies directly in this method. As of 25 April 2021, there were nine blockchain ETFs on the European market and ten blockchain ETFs on the US stock market. Among them, Grayscale Ethereum Trust (ETH) tracks the price of Ethereum, and Grayscale Bitcoin Trust (GBTC) tracks the price of Bitcoin. The other ETFs follow a basket of stocks that implement blockchain technology or digital assets. Another option is to invest in Coinbase stocks – the first listed cryptocurrency exchange with the second largest trading volume in the world and a market capitalization of US$59 billion.

F

Figure 3 (left): An investor buying ETH using StableCoin USDT on a cryptocurrency exchange

Figure 4 (middle): The hot wallet of ETH on the Binance platform

Figure 5 (right): C2C trading platform

Any Risks or Things that Need Special Attention?

Although you can use a credit card to buy cryptocurrencies on an exchange, the commission is high and the spread cannot be avoided. Another way is to first convert fiat money into StableCoins. One example is USDT, issued by Tether and matched with US dollars on a 1:1 basis with the exact amount in US dollars deposited in banks (i.e., the coins outstanding are the same as US dollars deposited in banks). The next step is to trade on the exchange using StableCoins, where the transaction price is much closer to the market price and the commission is close to zero. However, StableCoins and other coins in Hong Kong generally need C2C transactions, thus know your clients (KYC) and anti–money laundry (AML) are two issues you may face when buying or selling these cryptocurrencies. There have been cases of banks locking an account due to unknown cash flow, whilst bank accounts in the US and Australia have little problem in this respect (particularly when you withdraw money directly from an exchange).

Volatility in the cryptocurrency market is much higher than in the stock market. Recently, the US President was looking to increase the capital gains tax of the rich, as the cryptocurrency market has seen considerable fluctuations. Bitcoin fell around 20% in a week and Ethereum fell 12% in 24 hours. Traditional risk management can hardly work for the cryptocurrency market. In theory, the return distributions are likely to have heavy tails; as a result, the mean and the variance do not exist. The corresponding risk measures lose their statistical properties and the numbers are meaningless.

One traditional arbitrage strategy is calendar spread arbitrage – to bet that prices will converge for different futures or spot assets. My rough calculation of the “long spot asset, short future” strategy shows that you can obtain an annualized return of 30% in theory, however, with a high probability of receiving the margin call. The probability of receiving a margin call is close to 100% without frequency rebalancing (at hourly level). Note that the market is trading 24 hours a day and the margin call can occur in the middle of the night. If you do not use fully automatic trading and dynamic rebalancing, the strategy cannot generate any profit because of the extremely high volatility of the cryptocurrency market.

I hope that this short article has given you a better idea of cryptocurrency trading. On the one hand, trading cryptocurrencies sounds like pouring new wine into old wineskins, with the centralized exchange helping you to settle transactions; on the other hand, there are thousands of innovations in the trading mechanism. Investors should pay attention to market risk, operational risk, and credit risk (default in the cryptocurrency exchange occurs, whilst decentralized exchanges alleviate these concerns).

|

Financial Technology (FinTech) refers to the integration of digital technology with finance. FinTech disrupts the traditional financial industry through innovation in financial products, services, and solutions, as well as new business models and regulations. FinTech applies to finance artificial intelligence (AI), blockchain, cloud computing, and big data, supported by 5G and the Internet of Things (IoT). Hong Kong is proactively developing to become a leading international FinTech hub. Among various initiatives, the Hong Kong Monetary Authority (HKMA) issued eight virtual bank licences in 2019 and the city’s Insurance Authority (IA) granted four virtual insurance licences. A report issued by the Hong Kong Monetary Authority (HKMA) in December 2019 indicates that nearly 90% of the retail banks in Hong Kong have already used, or plan to use, AI in their business operations. There are currently more than 600 FinTech companies registered in Hong Kong. |

|

|

Dr Steven Wei Associate Professor School of Accounting and Finance |

To help Hong Kong develop its FinTech capabilities, the Faculty of Business (FB) at PolyU launched a Doctor of FinTech (DFinTech) programme in 2019, aimed at senior executives seeking to integrate academic studies with applied research and real practice to enhance their management and leadership skills in finance and other fields. The programme is currently recruiting its third cohort of students. It exposes students to the digital impacts of business with a focus on the financial industry and equips them with frontier knowledge in FinTech. The primary objective of the programme is to integrate academic studies with management practices to transform students into “scholar-leaders” in the FinTech field, focusing on digital technology, as underlined by the programme’s slogan “digital finance and beyond”. The core values of the programme are the following.

First, unlike traditional programmes that focus on a specific major, PolyU’s DFinTech programme is interdisciplinary and pools the resources of three faculties: FB, the Faculty of Engineering (FENG), and the Faculty of Construction and Environment (FCE). The professors who teach in the DFinTech programme are world-class academics and teach topical subjects in their areas of expertise, including Digital Economy, Accounting, Finance, Supply Chain Management, Management, and Marketing (FB); Big Data, AI, Blockchain, Cloud Computing, Cybersecurity (FENG); and Smart City (FCE).

Second, the DFinTech programme integrates academic studies, applied research, and management practices. In terms of research, various research centres and facilities at PolyU are involved in the programme, including the AMTD FinTech Centre of PolyU Faculty of Business, the University Research Facility in Big Data Analytics, and the Smart Cities Research Institute. These facilities are focused on applied research, with external partners such as AMTD, Microsoft, Alibaba, GogoVan, Huawei, and the Hong Kong Airport Authority. Students also enrol in the DFinTech Residential course, in which they can define their own business or management problems and develop digital solutions using the programme.

Third, to increase the international exposure and academic vigour of the PolyU DFinTech programme, students have the opportunity to participate in a digital transformation programme with the IMD Business School in Switzerland. After the 2008 financial crisis, many countries saw the value of FinTech development and the need for better data and more sophisticated data analytics capabilities.

As we move towards a digital economy, it is essential for senior executives to better understand FinTech and its impact on different industries, regardless of whether they work in large multinational corporations or in small and medium-sized enterprises. PolyU DFinTech will help them drive the digital transformation of their businesses and stay ahead of the digital economy trend. The programme also aims to contribute to the FinTech development of Hong Kong and the development of digital economy in the Guangdong-Hong Kong-Macao Greater Bay Area.